SIA Engineering (SIAEC), together with its parentco, has been badly hit by the pandemic. Its share price collapsed from S$3-4 levels to S$2-2.5 today. Years ago, I wrote an analysis with a bear case scenario that determined that the intrinsic value should be S$3.5 given that it will still earn S$200m of free cashflow (FCF) annually in a "downturn". My bull case has an intrinsic value of S$5 supported by annual free cashflow of S$250-350m!

SIA Engineer's five year share price

Well, the pandemic threw everything out of the window. SIAEC went into losses last year although it did continue to generate FCF, amazingly. This was S$150m in FY2020 (not to far off from my S$200m!) and S$80m for the first half of FY2021. So if we can get pandemic out of the way in 2022, then this can really be an interesting pandemic recovery play! But this is not post to gloat about the accuracy of my numbers. I am still in red by about 30% given my entry price was above $3. This is another "lesson learnt" post.

So what can we learn from this episode?

The first lesson, which has been said but not easily executable, was to cut loss or trim. When the pandemic broke out and all aviation names would be in trouble, there were opportunities to trim but I did nothing. I was cowering my head in the sand because it was too painful to face the situation and think. I should have written this post back then and come to the simple conclusion that trimming will give me firepower to buy more later.

Instead, I did other silly things are trimming winners and cutting other stocks that are less well-loved (only to see them rebound 100%). Yes, this name is one of my favorite, a rare Singapore stock. I couldn't bear to cut. This is the analyst's cardinal sin - do not fall in love with your stock. This is the second lesson.

Accelerating transformation!

Okay. Now that we have learnt our lessons, it is pointless the dwell on the past. It's time to look forward while remaining vigilant on how we can reshape our portfolios (the consistent message from SIAEC's investor materials!). There are two points to discuss: SIAEC's management and the future of aircraft maintenance.

This pandemic has reiterated the point that SIAEC's management is very good. They managed to steer the company into minimal losses and stayed FCF positive. Both the Chairman and CEO are recently appointed and yet they were able to lead decisively through the pandemic. As such, it means that the DNA of the firm is simply strong, capable of making the right decisions more often than not, allowing the firm to navigate the pandemic better than others.

The future of aircraft maintenance is harder to determine. Before the pandemic struck, one school of thought postulated that maintenance is in structural decline. Technology has improved and there is little need for expensive checks. More downtime means less time to fly passengers around. Well, with the pandemic, the trajectory has changed. There could be a strong recovery first before we talk about decline. But we also know air travel will not decline over the long run. The pandemic can stop us for two years, three years but not ten, fifteen years. Just look at Singaporeans traveling all over world the first chance we got!

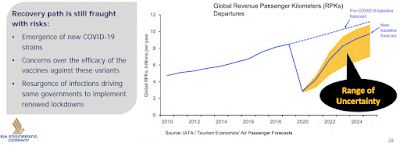

Recovery in sight but there is a range of uncertainty!

SIAEC's chart above showed management's view of the recovery trajectory. From this, we can tell that management is thoughtful about their business while the future remains uncertain. While passenger traffic can grow, maintenance could be a different story. The saving grace is that SIAEC has JVs all over the world generating c.S$4bn of revenue cumulatively (via its JVs and its own businesses on an annual basis) and was instrumental in its strong performance during the pandemic. So, even if the whole industry goes into decline, SIAEC can continue to gain share.

But let's not get too excited. Remember the cardinal sin? There is a recovery in sight but it will take a lot for SIAEC to go to S$5. After five years and losing a few thousand dollar and a little wiser, the new range of IV could be closer to $3-3.5. This is derived using FCF of S$150m and giving it 20x and add its S$500m on its balance sheet, its intrinsic value is c.S$3.5bn. With its share count of 1.12bn, this works out to be S$3.1. Using more optimistic no.s would put that to S$3.5. So we have 40-60% upside while the downside should be $1.6 (-40%) at the height of the pandemic.

I will be taking profit when it hits $3-3.5.

Happy Valentine's Day! Huat Ah!

No comments:

Post a Comment