This is one of those long awaited sequel post as we took time to discuss T bills and dividend stocks given the interesting market movements in the recent months. As mentioned in the past post, Security Analysis is this seminal book which provides good lessons for any investors but it's a bit difficult to read. But we can still learn a few lessons from it.

As promised, let's discuss the financial shenanigans and bad management which happened then (i.e. c.1920s) and will still happen as long as humans are greedy. As the gurus put in, the financial statements that will uncover financial shenanigans are usually the balance sheet and the cashflow. The P&L statement is the most straightforward and since most laymen can read it, shrewd management will not screw that up.

The balance sheet and the cashflow statements require more financial knowledge and it is the balance sheet that is used to hide the bad stuff. As such, the authors of Security Analysis warned against bloated balance sheets. By bloated, we are referring to account receivables, other assets, other liabilities and lines in the balance sheet that is used to hide the bad stuff.

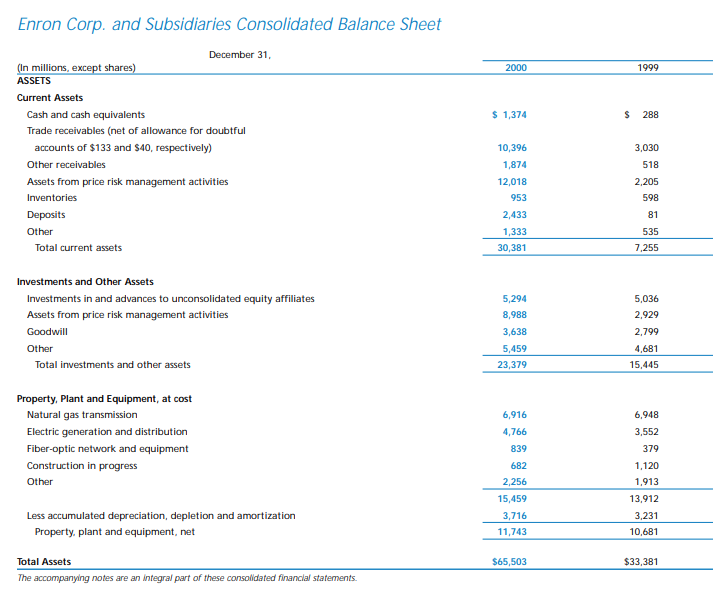

Most of the time, it is not easy to uncover because bad management has gone all out to hide stuff. I managed to find Enron's balance sheet in year 2000 online. Without hindsight, it is not easy to say things are wrong. The lines - "asset from price risk management activities" were where most of the bad was parked under, USD21bn worth of it, but management made so much effort to explain it so well that it's difficult to fault analysts for not being able to figure things out.

Bad management will never admit that they are bad so sometimes, in the end, it really boils down to gut feel. I have written about this on various posts in the past: Billon Dollar Whale Fraud Detection Lessons and Theranos, the fraudulent startup. To jot down a few tell-tale signs:

1. Bloated balance sheet, what we have we talking about so far

2. Keep talking about importance of secrecy, trade secret and know-how, trademark protection to mask the lack of disclosure

3. Lack of governance

4. Past issues with the law, including ongoing litigation.

As a side note, companies with litigation risks should also be avoided because the cost is simply to hard to measure. We discussed BP and Bayer in the past on this infosite. Both names did not recover past their previous peaks after the litigation mess broke out. BP was the infamous Deepwater Horizon accident and Bayer was ensued in the supposedly cancer causing Roundup fertilizer class action lawsuits.

In the next and final post, we discus other lessons learnt from Security Analysis.

Huat Ah!