In this last post on Security Analysis, we would discuss some of the difficulties analyst faced when analysing stock then and now. The authors have put some thoughts out elegantly which is worth studying here. Here are a few lines from the book, including one of the most famous line in full and in bold:

The market and the future present the same kind of difficulties. Neither can be predicted or controlled by the analyst, yet his success is largely dependent upon them both. The major activities of the investment analyst may be thought to have little or no concern with market prices.

The market is not a weighing machine, on which the value of each issue is recorded by an exact and impersonal mechanism, in accordance with its specific qualities. Rather should we say that the market is a voting machine, whereon countless individuals register choices which are the product partly of reason and partly of emotion.

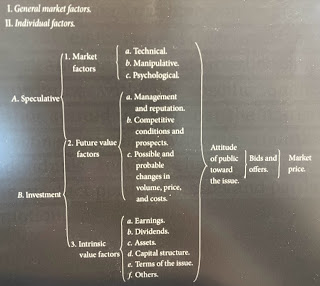

Alongside the famous line on the marketing being a voting machine, the authors also lay out this chart above to try to decipher what goes into determining market price. In short, there are so many things that make prices unpredictable in the short-term but yet it is the stock analyst's job to understand everything because in the long term, analysis of the business and its earnings power makes the difference.

Short term prices are also inexplicable but Wall Street wants actions and will explain for it, regardless whether the explanations are justified. This remains one of the hardest job of the day even for seasoned investors - to explain price action fo the day. Sometimes, stocks jump 5% for no reason and we only figure it out over the next few days.

Again, here are lines from the authors themselves:

The exaggerated response made by the stock market to developments that seem relatively unimportant in themselves is readily explained in terms of the psychology of the speculator. He wants action, first of all; and he is willing to contribute to this action if he can be given any pretext for bullish excitement (whether through hypocrisy or self-deception, brokerage-house customers generally refuse to admit they are merely gambling with ticker quotations and insist upon some ostensible reason for their purchases.)

Stock dividends and other favorable developments of this character supply the desired pretexts, and they have been exploited by the professional market operators, sometimes with the connivance of the corporate officials. The whole thing would be childish if it were not so vicious. The securities analyst should understand how these absurdities of Wall Street come into being, but he would do well to avoid any form of contact with them.

As such, in order to profit from stock investment, we come back to valuation. We cannot win trying to profit from short term market movement. The only logical way to win is to determine the intrinsic value of the stock and buy with sufficient margin of safety. The following paragraph, the authors cautioned that general market conditions ie beta sometimes overwhelm everything so we need to be careful.

Investment in bargain issues needs to be carried out with some regard to general market conditions at the time. Strangely enough, this is a type of operation that fares best, relatively speaking, when price levels are neither extremely high nor extremely low. The purchase of "cheap stocks" when the market as a whole seems much higher than it should be will not work out well, because the ensuing decline is likely to bear almost as severely on these neglected or unappreciated issues as on the general list.

On the other land, when all stocks are very cheap, there would seem to be fully as much reason to buy undervalued leading issues as to pick out less popular stocks, even though these may be selling at even lower prices by comparison.

On valuations, it was refreshing to see that the authors did lay out something concrete and also attributed the development to a certain Roger Babson (pic above), whom I didn't know who he was but apparently someone famous back then. The following is his rule of thumb:

The multipler might be equivalent to capitalizing the earnings at twice the current interest rate on the highest grade industrial bonds. The period for averaging earnings would ordinarily be seven to ten years.

In short, if the bond yields are at 3-4%, then earnings yield should be double of that at 6-8% and we should use the averaging earnings over 7-10 years. So we come back to why we should always buy stocks trading at teens price earnings, which can be difficult in today's context, so I would carefully stretch that to low twenties.

Last but not least, here's their words on wisdom on trading. In trading, there is no margin of safety, you are either right or wrong and if you are wrong you lose money.

The cardinal rule of the trader that losses should be cut short and profit safeguarded (by selling when a decline commences) leads in the direction of active trading. This means in turn that the cost of buying and selling becomes a heavily adverse factor in aggregate results.

No comments:

Post a Comment