When the pandemic broke out in 2019, we had no idea how crazy this could get. I have always been a fairly optimistic person and I thought we should be done in 12 months, if not 18 months. The world will quickly revert to normal because humans are creatures of habit and we like to go back to our old ways of lives as soon as we can. This is why losing weight is so difficult and why we cannot really change and become something we are not.

We are entering the third year into the pandemic now and things are not looking optimistic. New habits are now being formed which may replace old ones permanently. For instance, we may not need to meet everyone face-to-face going forward. Zoom or virtual meetings can easily become say 60% of all our meetings and old style phonecalls may still make up 20%. So the last 20% of face-to-face meetings will be saved for the most important, most precious counterparties.

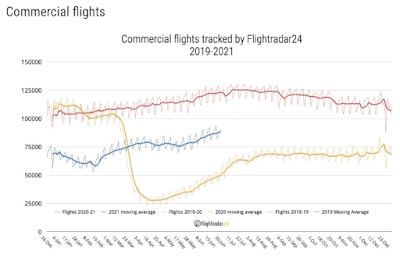

The big question is whether we will still fly as we used to. When the pandemic first broke, the airline industry quickly made a prediction: we will only get back to 2019's level of passenger volume by 2025. This was based on the experience from the 9-11 attack back in 2001. At first, I didn't want to believe that. We are so used to flying, how can that be true? Three years on, it now seemed likely, or perhaps, it could take even longer, since we are still only at 40-50% of 2019's levels.

Flight traffic comparison - courtesy of Flightrader24

This does not mean we will not travel anymore. It's the same as zoom or webex. We will save up for the best. We will still travel for leisure for sure. That's the first thing Singaporeans did! We are all not in Singapore now having not being able to travel for the last two years. Business travel should revert to some kind of new normal. For some, it could one less trip per year i.e. dropping for 4 to 3. For frequent flyers, it could be 10 to 8. But I believe, over time, we will surpass the previous peak. It is just whether it's 2025 or 2030.

It may be just numbers (of years) to most of us, but to the airline industry, it's big difference. Our beloved carrier SQ or Singapore Airlines (SIA), continues to burn around S$300m every quarter and if it is going to drag on, they will need money again (it raised S$8 billion last year). Similarly, aviation related plays will continue to be affected. It is amazing how SIA is now S$5 after a massive 50% dilution. At one point it was even close to S$6 which was just a tad away from the share price (S$6.4) before the dilution! How can the stock be diluted half revert to its old price in a matter of months, when the pandemic that caused the whole situation is still with us? Sometimes the market just doesn't make sense.

SQ continues to burn money

As such, my belief is that SQ is overvalued now, even if we actually start to recover now from COVID-19, we may not have enough margin of safety for this name. But for other SG stocks, there could be. One name that comes to mind is Jardine Cycle and Carriage, which I have also discussed previously. It has been badly hit by the pandemic and has not rebounded. Partially because it is operating in Indonesia, an emerging country will limited bargaining power for vaccines, medicines and with its domestic consumption still weak, with no recovery in sight.

Similarly, there are many recovery plays that could be interesting: restaurants, cinemas, domestic tourism names in other countries (not so much Singapore) and we should think hard to find these names. On the flipside of the coin, we should be worried about pandemic positive stocks, like zoom and other SAAS names, that had done really well. Some of them have already collapsed, but we may not see it bottoming yet because valuations are still sky high. Just look at Peleton (below), the Netflix + stationary bike manufacturer.

Peleton's share price

At the height of the pandemic, everyone wanted a Peleton bike. The market cap was a crazy US$50 billion. It has fallen 80% but still it's US$12 billion market cap, which is bigger than SQ! This is a company with no earnings, no track record, no cashflow. Just the idea that you can watch motivation exercise videos and cycle to lose weight, which was the best thing ever when everyone was stuck at home. But what happens when we can go out again?

We live in the most unusual times. The GFC created the new paradigm shift to zero interest rates which caused asset prices to inflate through the roof. Some of this huge monetary expansion finds its way to fund startups and created giants (Gojek, Tiktok etc) in the span of a few years. Then the pandemic hit and we saw how it accelerated the growth of some of these co.s but decimated segments of the old economy.

In the midst of all this, we now have real world inflation, a possible bubble of everything and potential recovery in some covid-hit names. But we have to exercise caution because all this is not going to end well. We can only diversify (not so much into cash but different holdings, perhaps even crypto - topic for another day) and hope for the best!

Happy 2022, huat ah!